Greetings to all readers of the HeatherBeaver online magazine! I’m with you again, Alla Prosyukova, one of the regular authors of the project.

My article today is relevant for all those who find themselves in a difficult situation due to the inability to pay off their credit debts in a timely manner.

You will learn:

- Who provides legal assistance to credit debtors?

- What kind of financial assistance can loan debtors count on?

- What should bank debtors do if they have nothing to pay the loan with?

In addition, I will offer a selection of reliable companies that can provide real professional assistance to credit debtors.

- Step 1. Select a company

- Tip 1. Start solving the problem as quickly as possible

What is help for credit debtors and when might you need it?

Most Russians know firsthand what a bank loan is. According to the Bank of Russia, about 38 million people have loans, half of them are people with credit cards.

The total credit debts of individuals amount to a little more than 10 trillion rubles, with overdue debt accounting for 10.5% of this amount.

All these credit debtors who have overdue debts need help first of all.

In addition to them, to one degree or another, assistance is also necessary for everyone who has loans, even those that are not overdue. They may need consulting support, help from specialists in developing a loan servicing plan, etc.

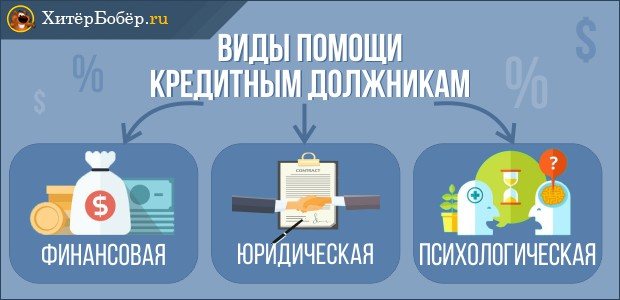

Help for debtors comes in different forms.

Help can come both from the creditor bank itself in the form of restructuring of an existing loan, and from other interested parties. For example, anti-collection companies that, under an agreement for a fee, are ready to assist the borrower in interacting with banks and debt collectors, and, if necessary, represent his interests in court.

You will find more details on the topic in the article “Loan debt”.

How do anti-collectors work?

It is necessary, first of all, to understand that an anti-collector is the same lawyer who has a highly specialized field of activity.

After the borrower contacts the anti-collector, they sign agreements.

The anti-collector finds out the details of the loan agreement and looks for loopholes in it, thanks to which it is possible to achieve a significant reduction in the loan payment amount.

In addition, if necessary, the anti-collector goes to court for financial compensation if the collectors put pressure on the debtor. Their responsibilities include:

- collection of audio and video evidence of unlawful actions of debt collectors;

- full legal support of the borrower until the loan is closed;

- developing a debt repayment plan together with debt collectors;

- attempt to restructure debt;

- compensation for material damage from collectors due to extortion.

What types of financial assistance are there for loan debtors - TOP 4 main types

There are several types of help for debtors.

Let's look at them in more detail.

Type 1. Loan refinancing

One of the most popular types of financial assistance for credit debtors is refinancing.

Refinancing is getting a new loan on more favorable terms from another bank to pay off an existing loan.

Let's consider the benefits that the debtor receives from such an event.

Example

In March 2020, Nikolay took out a loan from Sberbank for urgent needs in the amount of 300 thousand rubles. for 3 years at 19% per annum. Six months later, he had financial difficulties, and it became difficult for him to pay off the loan.

Nikolai began to look for options to ease his credit load. This solution for him was to refinance a Sberbank loan from VTB Bank at a rate of 15% for a period of 5 years. How much this helped him can be seen from the data in the table below.

Comparison of credit load before and after refinancing:

| № | Index | Payment on a loan received from Sberbank | Payment on a loan refinanced at VTB |

| 1 | Loan terms | 36 months | 60 months |

| 2 | Bid | 19% per annum | 15% per annum |

| 3 | Total payment per month | RUB 19,987 | RUB 7,137 |

We see that refinancing helped Nikolai reduce his loan burden by more than 2 times.

Now Nikolay will be able to conscientiously fulfill his loan obligations without any problems. If he has free funds, he can easily make both partial and full early repayment of the loan - the agreement provides for this possibility.

Type 2. Debt restructuring

Debt restructuring is the second, no less popular type of financial assistance to debtors.

Restructuring is a change by the bank to the terms of an existing loan based on an application from the borrower.

Let's look at the essence of this method using an example.

Example

Anna Mikhailovna, a 50-year-old woman working as a technologist at one of the factories in a small provincial town.

Her long-time dream was to take a sea cruise. The years passed, but the dream was in no hurry to come true. And then, for her anniversary, Anna Mikhailovna gave herself a gift - she bought a ticket to a Mediterranean cruise. True, my own savings were not enough and I had to spend 60 thousand rubles. apply for a loan from a bank.

The loan was taken out for 1 year at 14% per annum with a total monthly payment of 5,387 rubles. Anna considered this a completely acceptable price for her dream and began to look forward to the month of May to go on a cruise!

Time flew by quickly and now Anna is already returning home, rested and happy. But an unpleasant surprise awaited her at home. The entire staff of her workshop was sent on vacation with 2/3 of the average monthly salary retained for this forced downtime.

Of course, it became difficult to pay off the loan. In such a situation, Anna Mikhailovna turned to the bank with an application for restructuring.

Since Anna was a responsible borrower, the bank met her halfway and made a positive decision. The bank, in agreement with Anna, developed an individual payment schedule.

According to the new schedule, Anna pays off the loan in the amount of 1 thousand rubles within 3 months. instead of 5,387 rub.

After her solvency is restored, the woman will make a one-time payment in the amount of the entire accumulated debt during the easing period. Then Anna will again enter her standard schedule with the same monthly payments in the amount of 5,387 rubles.

Type 3. Obtaining insurance

When applying for a loan, the bank strongly recommends taking out insurance. It is assumed that insurance in the event of force majeure (serious illness, death, loss of work, etc.) should cover the debt. The borrower, when signing a loan agreement, is sure that if something happens, he will receive insurance. However, in practice everything is not so simple.

First, read the contract carefully. In 99% of cases, the beneficiary of the insurance becomes a banking institution, which means that the debtor cannot independently dispose of the insurance compensation for an insured event.

Secondly, even if an insured event occurs, the borrower will have to work hard and fulfill a number of requirements.

So, for example, if a borrower is insured against job loss under a loan agreement, then he needs to provide a work book, a certificate from the employment service, an insurance agreement, and a 2-NDFL certificate. All this must be done within 10 days after dismissal.

And the most important thing is that only loss of work at the initiative of the employer is recognized as an insured event; one’s own desire will not work here. However, in practice, situations often arise when an employer forces you to write a letter of resignation precisely at your own request.

Also remember that if you collect all the documents in full and on time, you will not immediately receive insurance; you will still have to wait for approval, and after receiving it, for the transfer of money from insurers. At this time, the growth of overdue debts, penalties and penalties will continue.

Type 4. Applying for a new loan from a private lender

Since ancient times, people strapped for cash have borrowed money from private individuals. These were not only acquaintances or relatives, but complete strangers - the so-called “loan sharks” who lent money at interest.

Now this method is becoming more and more popular, which is quite logical. Getting a bank loan is becoming more and more difficult. You need to collect a bunch of documents, sometimes collateral or guarantors are required, your credit history is checked, and it’s not a fact that the loan will be approved in the end.

And if the borrower is in arrears on the loan, then solving the problem becomes even more difficult.

The entire Internet is full of advertisements from private lenders. The offers are very tempting: within a few hours, against a notarized receipt, and sometimes just against a receipt, according to 2 documents, at an acceptable percentage, you can get a decent amount - from 5-10 thousand rubles. up to several million.

However, I want to warn you right away - there is a great chance of running into scammers.

Therefore my advice to you:

- choose a private lender through special online services that have a service that checks lenders registered on this resource;

- never take out a private loan against collateral;

- refuse offers that require any advance payment, even the smallest;

- take out loans from private individuals only in case of emergency.

Very often, credit borrowers, due to the difficulties that have arisen, are in a depressed state, under pressure from creditors. In this state, they need not only professional legal assistance, but also psychological support.

A credit debtor can find such support both from professional psychologists and from anti-collection companies, whose specialists, along with their basic services, involuntarily provide psychological assistance, reassuring the borrower and instilling hope for a possible positive resolution of his problem.

What are the risks of defaulting on a loan?

By signing a microloan agreement, the client undertakes to fulfill all the conditions of the lender: repay the loan on time, pay interest and fines in case of delay.

An MFO can carry out its activities by obtaining a license from the Central Bank. After the license is issued, the microfinance organization is included in a special register. If the name of a microfinance company is not in the register, this means that it operates illegally. In this case, the company will not be able to go to court to collect the overdue debt.

I sign the contract, each client must understand that:

- an electronic contract has legal force, on par with one signed in person in the office;

- the debt will have to be repaid;

- when applying for a long-term loan, MFOs do not remind about the repayment date of the mandatory contribution;

- if there is a delay, the companies continue to charge interest under the contract and penalties;

- in case of delay, MFO specialists have the right to call the debtor or contact persons, send requests for repayment via SMS messages or email;

- In case of prolonged non-payment, the case is referred to court.

Attention! If your salary is delayed, you can get an interest-free loan and pay off the current debt. However, don't get carried away. You can apply for a loan without interest here.

How to get help for loan debtors - step-by-step instructions

If the situation with your credit debt is critical, if you need professional help, but you don’t know where to start and where to turn, read our instructions.

In it you will find a step-by-step algorithm of actions.

Step 1. Select a company

There are now many anti-collection agencies and simply law firms ready to take on the solution of credit problems and provide assistance to debtors.

When choosing a company, read reviews about it on forums and specialized websites. Explore the company's website. If it does not contain information about the company itself or any useful information materials, then it is better to refuse the services of such a company. A serious company pays great attention to its corporate resources.

Perhaps the company is a rating participant in its field. Check them out.

Choose a company that has been operating in this area for quite a long time and has a proven track record of winning cases.

When choosing a company that should help you get rid of credit problems and headaches about this, save your nerves and money, do not be lazy to collect as much information as possible confirming its professionalism and business reputation. Remember: the success of the entire event depends on this.

Step 2. We provide the specialist with the necessary documents

After analyzing the reviews about the candidate company, reading the website, list of services and general terms of cooperation, you have made your final choice.

Having chosen a company, prepare the necessary package of documents. As a rule, you will need to submit all documents relating to the loan agreement in which there are problems.

An approximate list of required documents:

- loan agreement with all attachments;

- collateral documents (if any);

- correspondence with the creditor bank or collectors (if any).

After reviewing the documents, the credit lawyer will be able to draw preliminary conclusions about the complexity of the problem and the prospects for solving it. The specialist will offer all possible solutions to the problem in this situation. This will allow you to choose the most optimal one.

Step 3. Conclude an agreement

After the main points have been agreed upon, it is time to conclude the contract. I suggest you familiarize yourself with an example of such an agreement.

Read all of its points carefully. Watch what you sign. Pay special attention to the point “responsibility of the parties”. Often, such a clause is simply missing in contracts for anti-collector services, and this should alert you. A company that operates honestly is not afraid to take responsibility.

In contracts you can find wording that by paying money for the current month, the customer confirms that the services for the previous month were completed in full and has no claims against the contractor for this period. However, in this section there is not a word about a document that can confirm the scope and list of services provided.

Such a document can be a (detailed) act on the services provided, or a brief report containing all the necessary information. Demand that such a clause be included in the contract if it is missing. This will allow you to control the performer and increase his responsibility.

Step 4. Pay for services

Anti-collector services can be paid either one-time or in the form of a subscription fee. In case of a one-time payment, the client must make it for each consultation or other service provided.

When paying for a subscription, the client pays a monthly fee as a percentage of the amount of credit debt (usually 1%). Cooperation between a debtor client and an anti-collection company can last up to six months.

In addition, client representation in court is paid separately. The cost of such a service is approximately 5 thousand rubles. There are usually several court hearings.

You can pay for services both in cash and by non-cash methods.

Step 5. Get a detailed action plan to resolve the problem

Anti-collector services are provided in 2 stages: pre-trial and representation of the customer-debtor in court.

During the pre-trial stage, the lawyers of the executing firm perform a number of activities.

Some of them:

- analysis of the debtor's state of affairs;

- development of solutions to the problem;

- calculation of the client's debt and comparison with data received from the creditor;

- preparation of documents to resolve the situation;

- interaction with the bank or collectors.

If the desired result is not achieved at the initial stage, the problem will have to be resolved in court. In this case, the customer will be required to have a power of attorney for the anti-collector to represent the client’s interests at court hearings.

When you need help from microloan lawyers

So, are you thinking about taking out a short-term loan? You will need legal assistance on microloans to check:

- location of the subject in the state register;

- whether the lender has the right to issue loans (permitting documentation);

- the possibility of a microloan organization using illegal methods to repay a loan.

To obtain information of interest, as well as information on how to take out a loan correctly, what you need to pay attention to when formalizing a credit relationship, sign up for a free consultation by filling out the form on the website.

If you are already a debtor to a microfinance structure, then the help of microloan lawyers is necessary for:

- imposition of sanctions by the creditor;

- receiving threats against the borrower and his family members;

- use of blackmail by representatives of the lender;

- the implementation by the lender's employees of actions that discredit the borrower;

- dissemination by the creditor of false information about the debtor;

- damage to property;

- an immediate threat to the health and life of the borrower and his loved ones;

- the client is in a difficult financial situation and understands that late payments cannot be avoided;

- other unpleasant circumstances.

If at least one of the above situations occurs or there are other complaints, contact the online consultant by filling out the appropriate form and receive answers online.

What to do if you can’t pay the loan - 3 simple tips

Life circumstances can turn even the most responsible borrower into a defaulter.

What to do in this case? Read our tips.

Tip 1. Start solving the problem as quickly as possible

“Our problems will not disappear because we close our eyes and stop looking at them,” said Winston Churchill many years ago.

Don't turn a blind eye to the problem of lack of funds to pay your credit debts. The sooner you start looking for a way out of this situation, the faster you will find it.

Consider whether you can borrow from your friends, relatives or acquaintances.

Perhaps your credit history will allow you to refinance on acceptable terms, look for options. Just don’t throw yourself into the pool headlong.

Refinancing can only be considered if:

- the terms of the loan do not worsen your current situation;

- the amount of the new loan will completely cover the existing debts.

Remember, the faster you begin to solve your problems, the more fines and penalties you can avoid.

Tip 2. Be the first to contact a bank or collection agency

At the first sign of your financial insolvency, go to your bank or to collectors if the loan has been assigned to them. Explain the situation, ask for help in solving the problem.

As practice shows, in most cases, creditors agree to a meeting. Neither the bank nor the collectors are attracted by the prospect of you having overdue debt, which from current can very quickly turn into long-term, and possibly even hopeless.

You may be “frozen” on interest payments for quite a long period of time and then you will only pay the principal amount. Or the bank will agree to provide you with a credit holiday. They can last up to 3 months. During this time, you can find an additional source of income (part-time work), sell unused property, etc.

Tip 3. Engage a professional lawyer

If you do not have enough experience in solving financial problems, you are poorly versed in the law, then the services of professional lawyers, for example, from an anti-collection agency, may be your solution.

An experienced anti-collector, having studied your situation and documents, will be able to find a legal solution to the problem. A timely contact with professionals will not only allow you to get out of the credit web, but will also save you nerves.

Watch the video to see how to help yourself get rid of debt.

What to do if the debt was transferred to collectors?

In most cases, microfinance organizations sell debt to collectors. Since debt collectors are interested in getting their money back, they offer a discount. Its size is agreed upon personally.

What does the discount depend on? The answer is simple, from the redemption value of the debt. For example, Matvey Ivanov has a debt to the microfinance organization in the amount of 37,600 rubles. The company sold the debt to the collector for 21,000 rubles. Collectors can offer a discount of 37,600 – 21,000 = 16,600 rubles. Just don’t hope for the maximum right away; this is relevant for problem borrowers who have not paid their debt to the collector for months. In practice, the discount amount is up to 10% of the debt to the microfinance organization.

An example from life! Olga Matveeva took out a loan for 17,000 rubles, ended up in the hospital and was unable to pay off the debt. A month later she was discharged, but the amount of debt increased to 27,200 rubles. Since Olga did not have the full amount to pay, she tried to resolve the issue with the collectors who were involved in collection. I was lucky that it was New Year's Day in a week. Olga was offered to return 80% of the debt. She paid 21,760 rubles (the amount was 340 rubles less than the planned loan repayment).

Which microfinance organizations definitely sue borrowers?

Despite the fact that prosecution is quite rare, there is a list of companies that resort to this method of influencing the client. Among them:

- Turboloan;

- Moneyman;

- Webbanker;

- UrgentMoney;

- Zaimer;

- Viva money.

These are large companies that have been providing microcredit to the population for a long time and operate within the existing legal framework. In most cases, they give up to 3–5 months, during which the debt issue can be resolved without going to court.

If you cannot repay the loan on time

Microfinance organizations are aware that they work with a riskier category of borrowers who may face financial difficulties. That is why many companies have introduced extensions to their line of services.

Extension is an opportunity to shift the loan repayment period for a certain period (a week, several weeks, a month). At the same time, the borrower avoids fines and his credit history does not deteriorate. The conditions for granting a deferment of the payment deadline are the absence of delay and payment of accrued interest (only the principal debt is subject to deferment).