Often people take out various loans without first assessing their own solvency and financial condition. This results in them incurring significant debt. This is the basis for the bank to start collecting funds in different ways.

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem, please use the online consultant form on the right or call.

It's fast and free! The process can be implemented using different methods, but most often, bank employees try to contact the debtor and his relatives through telephone calls.

When bank employees start calling

The bank starts trying to contact the debtor literally a few days after the delay occurs. If the required amount of funds does not arrive in the account on the appointed date, then the institution’s employees begin to try to contact the debtor by calling the debtor. Usually the phone number is indicated in the application form.

Target

The main goal of the institution’s employees is to obtain information about why funds were not received on the appointed date. It is advisable to calmly explain to each payer the reason for the delay.

If a person was fired, fell ill, or his salary was delayed, it is advisable to immediately inform the bank employees about this. An employee of the organization will ask when the funds will be deposited, and he will report that fines and penalties have already been assessed.

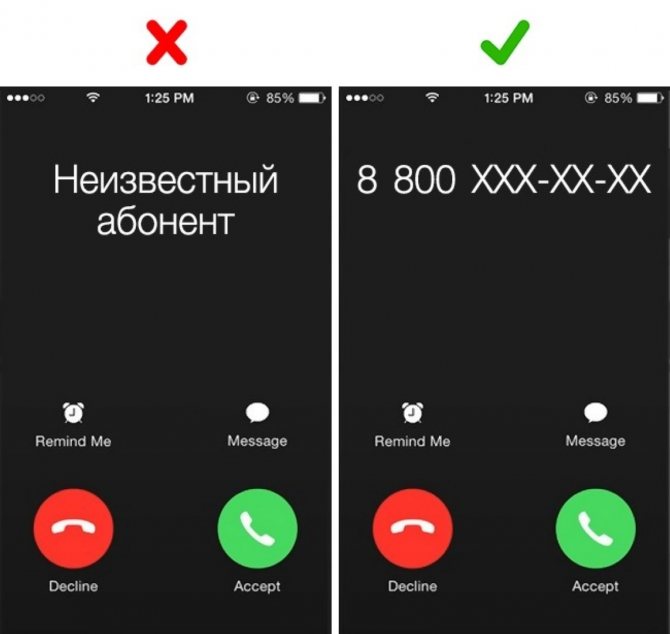

The bank will not call from an unknown number.

Another purpose of the conversation is to inform the debtor about exactly what amount he should pay.

Why does this happen all the time

If the debtor does not repay the loan, the bank begins to use various enforcement measures. Constant calls from employees of the organization act as a psychological measure of influence.

People begin to get annoyed by such calls, so they try in different ways to pay off the debt in order to stop communicating with the organization’s employees. Calls usually continue daily until the loan balance is paid.

Can the bank call

These organizations have every right to take such measures, although the law has restrictions on the time and number of calls. Therefore, the following requirements are taken into account:

- It is not allowed to call debtors at night or early in the morning, but usually bank employees do not make such mistakes, so they do not violate the law so flagrantly;

- if there are constant calls at any time of the day, then it can be argued that the debt was sold to collectors;

- During communication, you can ask who exactly is calling and what organization they represent.

If the person calling does not introduce himself or indicate which bank or company he works for, you can safely hang up.

Consequences of refusal to answer

Many debtors, if they are in arrears, prefer to simply stop picking up the phone. Such a decision may cause the bank to try to contact relatives or colleagues of the debtor so that they influence him.

When filling out an application for a loan, you are usually required to provide contact information for relatives, so these phone numbers are used by employees of the organization to influence the citizen.

Communication with relatives

Calls to the debtor's close people act as a certain measure of influence. It is assumed that when a person’s family finds out about his debts, his relatives begin to constantly ask about his problems, force him to pay off his debts, and often even financially help him cope with his problems.

What to do if the bank calls about someone else’s loan, this video will tell you:

If the bank continues to call relatives every day, then this begins to irritate them, so they begin to influence the debtor more effectively.

Calls to work and responsibility

When filling out an application for a loan, the citizen’s official place of work must be indicated. If calls to the borrower himself and his relatives do not bring the desired result, then the bank may start calling the debtor’s work.

Such a tool of influence is effective, since bosses usually have a negative attitude towards information that their employees are negligent loan payers.

Usually it is collectors who call at work, not employees of a banking institution, but such actions are illegal, as they involve the dissemination of personal data, so you must file a complaint with Roskomnadzor.

If bank employees actually begin to communicate with the debtor’s management at work, then this is a serious violation, for which significant fines of several tens of thousands can be imposed by the court.

But judicial practice on this issue quite often contains cases where the court took the side of the institution, so it was not held accountable.

When are bank calls to third parties legal?

The law allows calls to the debtor’s relatives in several situations:

- when filling out the form, the borrower independently indicated the telephone numbers of his family members for contact in case of need;

- a relative is a guarantor or heir of the debtor;

- It is impossible to contact the borrower himself in any way to convey important information about the loan, so communication with a relative is the only way to do this.

Should you be afraid of bank calls? Photo: onfinanson.ru

If the bank can prove the above situations, then the court will not be able to hold it accountable for constantly calling the borrower’s relatives.

Debt collection without court (by writ of execution from a notary)

Law

The provision on extrajudicial debt collection is included as an amendment to the law “On Amendments to Certain Legislative Acts of the Russian Federation (in terms of clarifying provisions on property valuation issues).” The changes also affected the laws “On Insolvency (Bankruptcy)”, “On Valuation Activities in the Russian Federation” and “Fundamentals of the Legislation of the Russian Federation on Notaries”. Adopted by the State Duma on June 22, 2020 and approved by the Federation Council on June 29, 2020. Since July 2020, banks have been allowed to collect some debts based on a notary’s writ of execution without a court decision and contact bailiffs directly. Apparently, banks will actively use these opportunities, since it is quite expensive for them to go to court for each of the non-repaid loans. Moneyiformer summarizes important innovations.

What debts are we talking about?

Before the adoption of the June 2020 amendments, it was already allowed in an indisputable manner - by a notary's writ of execution - to collect debts to pawnshops (under a pawn ticket) and under storage and rental agreements.

This right now extends to:

— For all overdue payments and loans under loan agreements, which directly or in additional agreements stipulate the conditions for the possibility of debt collection under a notary’s writ of execution. — Notarized transactions establishing monetary obligations or obligations for the transfer of property; — other documents, the list of which is established by the Government of the Russian Federation.

Not subject to indisputable collection without going to court

— Debts under agreements with microfinance organizations. — Mortgage debts. (According to the mortgage law, there is a ban on extrajudicial foreclosure of residential premises owned by individuals). — Debts for housing and communal services (such agreements are not notarized).

In addition to the debt itself, interest is collected

If the accrual of interest is provided for in the contract, then they are also subject to collection. In addition, the amount of expenses incurred by the claimant in connection with the application to the notary, as well as the penalties provided for in the contract (except for the amounts of penalties under loan agreements), are recovered.

Collection process

— Two weeks before applying to a notary for a writ of execution, the credit institution is obliged to notify the debtor of the existence of a debt. — The notary must be provided with documents confirming the indisputability of the claims against the debtor, as well as a copy of the debtor’s notification that he has an overdue debt. — At the request of the claimant, the notary makes a writ of execution. This will be done in the absence of the debtor, whom the notary will subsequently notify that the collector has the right to contact the bailiffs to collect the debt. — Having received a writ of execution on documents that confirm the existence of an agreement and overdue debt, the creditor transfers the documents to the bailiff service. — The basis for debt collection for bailiffs will be the notary’s writ of execution on the borrowing agreement.

Important points of the procedure

— The debtor’s disagreement will not in any way affect the collection procedure under the writ of execution, however, the debtor can challenge it in court. — The debt for which pre-trial collection is carried out must not be older than two years. — Banks now have the right to contact a notary for a writ of execution immediately after a loan payment is overdue. At the same time, according to Law No. 353 “On Consumer Credit (Loan),” loans that are overdue for more than 60 calendar days within the last 180 calendar days are subject to early repayment. Most likely, banks will adhere to these deadlines, and this procedure will primarily affect borrowers who have not paid for more than two months, and who have also violated the payment schedule before. — Debt collection without going to court under loan agreements concluded before the adoption of the law will become possible if the lender and borrower sign additional agreements to the existing agreements in which this condition is present. — A new concept is introduced into the law - “liquidation value” for alienated property, and the rules for conducting auctions of alienated property of the debtor are also changed. — For debtors, collection based on a notary’s writ of execution, which essentially replaces a court decision and subsequent appeal to collectors, can be a positive factor. Bailiffs act in accordance with the law, but collectors do not always.

How to talk correctly

If employees of an institution call regarding an unpaid loan, then the debtors themselves should know some recommendations regarding proper communication with specialists. These include:

- you should not give in to panic;

- you need to communicate politely and calmly, since insolence and rudeness can only aggravate the situation;

- It is not recommended to make groundless promises or disclose information about yourself and your relatives;

- it is important to find out which agency employee is calling the citizen, as well as on what grounds this call is being made;

- It is advisable to install a program on your phone in advance that records conversations, since if the caller violates the rights of a citizen, he will be able to use this recording in court if necessary.

Thus, with proper communication with bank employees, you can prevent violation of your rights.

Where can I complain?

If employees of the organization call too often, or at night, then you can file a complaint against the bank to different authorities:

- if illegal methods of influence are used, then you need to contact the police, and you can also write a statement to the prosecutor’s office;

- if the calls continue at night, and also if the callers threaten the debtor in the conversation, then it is necessary to file a statement with the police;

- if extortion by bank employees is detected, then you must contact the Investigative Committee;

- If personal information is used illegally, you must file a complaint with Roskomnadzor.

How to talk to a bank, watch the video:

For any person, calls about the need to repay a loan are unpleasant and annoying, but at the same time they are legal, so in most cases banks do not violate the law, so borrowers themselves are required to comply with the law and responsibly treat loan repayments.

Statute of limitations

If the bank suddenly stops calling and demanding the return of borrowed funds, perhaps the reason lies in the fact that the statute of limitations on the loan taken has expired. In Art. 196 of the Civil Code of the Russian Federation stipulates that it is three years. However, at what point do you start counting? The answer to this question is contained in Art. 200 Civil Code of the Russian Federation. In relation to the relationship between the creditor and the borrower, the limitation period begins to run from the day when the person should have learned or learned about the violation of his rights, that is, from the moment the creditor discovered the fact of late payment.