The struggle for the client, fierce competition in the financial market, distribution of easily accessible banking products, advertising slogans “Take a loan, live beautifully!” generated a huge number of problem borrowers.

Professional debt collection and who the collectors are, why banks interact with them, what rights the debtor has is a hot topic for discussion.

Who are collectors? ↑

Collector literally means “gatherer.” Collection agencies are organizations specializing in collecting debts from individuals and legal entities.

Their goal is to use any methods (mainly psychological pressure) to force and stimulate the debtor to repay the debt.

Unfortunately, today there is no special law regulating the activities of collectors. Their activities are regulated by criminal law (extortion, battery, intimidation, arbitrariness) and the Civil Code.

Typically, companies that have a huge number of such debtors and cannot cope with this category of clients on their own resort to the help of specialized agencies.

These are banks, microfinance organizations, insurance companies, utility organizations, etc.

Do you want to get a microloan without refusal with a bad credit history? We recommend that you read the article dedicated to this issue at the following link. You can find out how to take out a microloan online to a bank account without refusal by following the link.

Is it worth answering letters?

Many people are tormented by the question. Is it worth answering such letters? There is no clear answer. If the letter did not arrive by mistake and the person owes something to one or another banking organization, then you should contact a qualified lawyer and draw up a plan for communicating with debt collectors and not deviate one step from it. No psychological breakdowns or hysterics are accepted (this is precisely the goal of collection agency employees in order to throw a person off balance and force him to pay mythical bills).

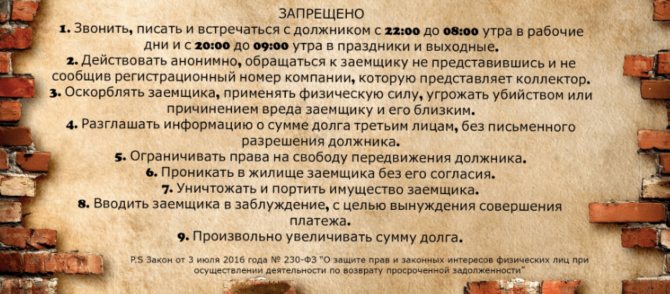

What prohibited methods are used? ↑

In fact, there are many prohibited techniques that collection agencies use.

Most of them come down to psychological pressure on the debtor; we suggest you familiarize yourself with just a few of them:

- calls to the debtor’s work (colleagues, superiors) with information about debt that compromises the person;

posting leaflets and photos with information about the debtor and his debt on the entrance, windshield of a vehicle, and other places;

- visits of collectors to relatives and neighbors of the debtor;

- posting notices in public places allegedly on behalf of the debtor stating that he owes a certain amount of money to the bank;

- sending false notices, letters, etc. on behalf of the executive body, court, police, etc.;

- blackmail, intimidation of the debtor and his family members;

- confiscation of property;

- causing bodily harm.

With such methods of influence, the debtor must immediately contact law enforcement agencies to eliminate this situation.

Collectors spoke about the reasons for debtors’ refusal to repay loans

Russian debt collectors shared details about the reasons used by Russians who refuse to pay their loans. The main one is lack of money. Some citizens do not agree with the amount of debt and seek to prove their case in court.

The National Association of Professional Collection Agencies (NAPCA), which unites 38 market participants, conducted a survey of Russians who are in default on various types of loans and found out what reasons force them to avoid repaying their debt. The survey involved about 1 million debtors who were interviewed by telephone. The results of a study conducted in 2020 were published by RBC. Only those debtors who refused to return the money participated in it.

The survey was conducted as follows: representatives of collection agencies called debtors whose phone numbers were in their database and asked them whether they planned to repay the overdue debt. If the defaulters refused to do so, the collectors recorded the reason for the refusal.

As NAPCA notes, collectors are currently working on about 6.5 million bank debts worth more than $1 trillion that have been assigned to agencies.

Nothing to pay with

First of all, as the study showed, the main reason why Russians refuse to repay borrowed funds is the financial difficulties that debtors encounter. This answer was given by 47 percent of the debtors surveyed. Moreover, 30 percent of those who gave this answer do not want to pay off debts because their own incomes have fallen. Another 20 percent of debtors with financial difficulties indicated that they were unable to cope with their current debt load. 18 percent cite job loss. 17 percent indicate that they cannot service their debts because prices in stores have increased dramatically, and this has hit their budget. About 10 percent of defaulters admitted that they had recently encountered large expenses for a vacation or some unplanned purchases, and therefore were temporarily unable to repay the loan. Another 5 percent of people who do not have money to pay debt explain this by family circumstances.

The court will sort it out

The second most popular reason for not paying loans is the debtor’s disagreement with the amount of debt assigned to him. 13 percent of Russians refuse to pay a loan with precisely this motivation. Another 9 percent of respondents believe that the court will help them achieve a reduction in the amount of payment, and are ready to defend their opinion in court. 7 percent of respondents believe that they will not need to repay the money they borrowed at all. Another 7 percent did not initially understand the conditions under which they were given a loan, and 4 percent of respondents are not aware of how a loan that was overdue is paid.

As NAPCA points out, the number of defaulters who deliberately bring their case to court, hoping that they will be acquitted, is gradually increasing.

As a rule, the court is a last resort to which the confrontation between the creditor and the debtor comes. It comes into effect if all attempts to reach an agreement peacefully have had no effect. In accordance with the law on the protection of the rights of individuals when collecting overdue debts, four months after the delay arose, the debtor has the right to refuse to interact with the creditor, that is, the bank or its representative, represented by the collector. If the debtor exercises this right, the court remains the only way to collect the debt from him.

On this topic

2226Samoilova spoke about the reasons for refusing to divorce Dzhigan

Russian model Oksana Samoilova said that she had not forgiven her husband, rapper Dzhigan, however, she refused to divorce him in the interests of their four children.

As the general director of the collection agency “M.B.A.” points out. Finance" (part of NAPKA) Fedor Vakhata

, from actual judicial practice it follows that in most cases in litigation between debtors and creditors, the court takes the side of the latter.

Another expert, legal director Leonid Fainberg

, points out that banks have legal departments whose task is to thoroughly prepare for court hearings. Thus, the creditor usually provides a comprehensive amount of documentation confirming his case, and the court rules in his favor.

We will work in kind

Earlier, in the fall of 2020, the center of the National Agency for Financial Research conducted a survey of Russian citizens, asking its participants how they felt about late loan payments. According to the results, more than a third of respondents (38 percent) answered that they do not see anything wrong with a slight delay in payment. 8 percent, in turn, said that, in their opinion, it is acceptable to completely refuse to pay off debts under any circumstances.

As for the NAPCA study, it follows that debtors in some cases are still ready to repay their debt that was overdue. True, they offer to pay not in money, but in kind. In particular, as options for repaying it, they are considering the possibility of working off the required amount, for example, by making repairs to the creditor or going to work as a security guard on night shifts, paying off the debt with vegetables and fruits grown on their own plot, or pets, returning the money through a tax deduction or securities they hold.

Earlier, the head of the Federation Council, Valentina Matvienko, announced the need to ban in Russia the issuance of loans by microfinance organizations secured by residential real estate.

What's legal? ↑

Borrowers who, for some reason, were unable to repay the loan on time, are always interested in what are the legal methods of work of collectors?

In fact, there is no law regulating collection activities today. The Civil Code and criminal law help regulate the relationship between the collector and the debtor.

All legitimate work of collectors comes down to psychological impact on the debtor. This manifests itself in phone calls (from 6-00 to 22-00), SMS, letters.

Do you want to know which bank has the lowest interest rate on a consumer loan? Read our article. Where to get a microloan without refusal and without verification instantly through the Contact system, read here.

You can learn more about microloans without refusal for pensioners under 76 years of age using the link provided.

You can come to the debtor’s place of work or home only with the borrower’s prior consent.

Moreover, loan information cannot be disclosed to third parties. And it is worth remembering that debt collectors cannot threaten or injure. But some collection agencies, especially those who do not value their reputation, resort to prohibited methods.

Do I need client permission?

Article 382 of the Civil Code of the Russian Federation does not provide for the obligatory consent of the debtor to sell the debt to a third party. It is sufficient if the loan agreement states that the borrower agrees to the transfer of personal data to a third party. As a rule, this assumption is a standard clause in the lending agreement.

The nuance of this rule is that the lender is obliged to notify the borrower of its intention to sell the debt to a third party. If this is not done, the borrower has the right to continue fulfilling obligations (debt repayment) to the original creditor.

In the case where the sale of the debt occurred after the transfer of the writ of execution to the bailiff, the responsibility for notifying the debtor of a change in the person in the obligation rests with the FSSP. At the same time, the debt repayment scheme agreed with the bailiff does not change. The new creditor, if a collection agency becomes one, does not have the right to demand a change in this scheme.

What can collectors do to the debtor’s relatives? ↑

Quite often, relatives of debtors complain that collectors start calling them, several times a day (on a cell phone, work, home landline), demanding to repay the debt or in some way to influence the borrower.

This method of “knocking out” a debt from a borrower is outside the law:

- Firstly, disclosing information about a loan to third parties is not permissible.

- Secondly, relatives (even the closest ones) are not responsible for the loan that was issued by the debtor.

If relatives start receiving calls, we immediately recommend that they contact the police with a complaint of extortion.

The debtor may also write a statement to the appropriate authorities regarding the disclosure of information to third parties.

Is it possible to be held accountable?

If collectors actually violate the conditions and requirements of the law during work, then, if there is evidence, they can be held accountable.

The following methods can be used for this:

- filing a statement with the police, to which are attached records, documents or other documents confirming the unlawful actions of debt collectors;

- transfer of the complaint to Rospotrebnadzor;

- filing an application with the prosecutor's office.

What can't debt collectors do?

Practice shows that such cases are considered even by the police superficially, so collectors are rarely actually prosecuted.

What should a debtor do if collectors start making threats? Find out here.

This is because such claims are numerous and complicated by the fact that agencies also have evidence that they are acting legally.

Therefore, many debtors understand that various complaints and statements are truly useless.

What prohibitions exist? ↑

You must know and remember that, according to current legislation, collectors are prohibited from:

- remind yourself (come, call) from 22-00 to 6-00;

- speak to you on behalf of law enforcement;

- threaten you, relatives, acquaintances, colleagues;

come to the address where you live or work without prior approval (moreover, it is prohibited to break into a house or office);

- transfer information about the debtor to third parties, for example: work colleagues, management, neighbors, acquaintances, etc.;

- provide knowingly false information about the amount of debt, penalties, fines, etc.;

- carry out any actions against the debtor that are contrary to current legislation.

If any action is taken by the collector as described above, immediately call the police and file a report.

What debts does the bank sell to collectors?

The decision to sell debt to a collection agency is made by the bank independently based on their internal credit policy towards clients and correspondents. First of all, they strive to get rid of small debts, the costs of collecting which are comparable to the costs that the bank will be forced to incur if it does this on its own. This takes into account:

- amount of debt;

- the financial condition of the borrower at the time of applying for the loan;

- the presence of collateral, guarantors or co-borrowers;

- location of the debtor;

- his desire to make contact with the creditor.

The smaller the loan amount, the higher the likelihood that when payments stop, the bank will sell such debt.