How to write to a bank about debt restructuring

No one is immune from financial problems. If such problems overtook you at a time when you have loan obligations to the bank, there is no need to panic or hide, there is a way out - debt restructuring. In order for the bank to consider this option, you must notify it in writing of your concerns.

You can write a letter in free form, but it must reflect the main points:

- date of receipt and loan amount;

- at what point did you start repaying the loan, how much have you repaid so far, how much do you still have left to pay;

- from what moment did you stop paying the loan in accordance with your obligations;

- What kind of financial difficulties are you experiencing? This point needs to be written down - on its basis, the bank will make a decision on exactly how best to restructure your debt (offering you a “credit holiday” or increasing the loan term by reducing the rate);

- what amount are you willing to pay monthly under the new conditions.

You need to write two copies, take them to the bank, register them and wait for an answer.

Debt restructuring agreement

The debt restructuring agreement is aimed at easing the borrower's credit burden and at the same time ensuring full repayment of the debt, including interest.

The agreement specifies all the main points regarding debt restructuring. In particular, the chosen restructuring scheme:

- "credit holidays" The borrower pays only interest on the loan, payments on the principal debt are postponed for a certain period (determined by the bank);

- currency replacement. Not a very popular option, which is not surprising given the sharp jumps that can be observed recently in the foreign exchange market;

- change in the interest calculation scheme: equal payments change to a monthly decreasing amount. Or vice versa;

- reduction in interest rate. It becomes possible when the loan agreement is extended.

New loan terms come into force from the moment the agreement is signed.

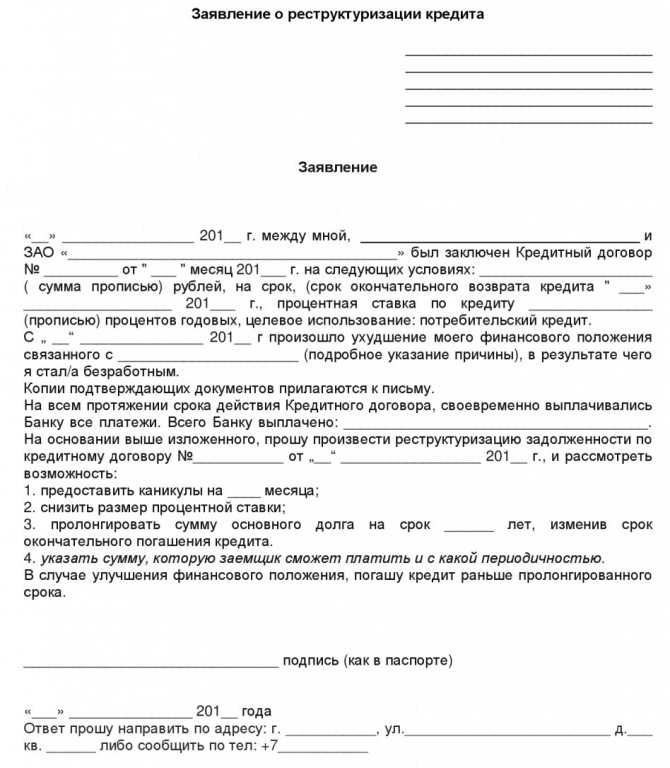

Application example

On April 12, 2020, between me, Petrov Petrovich and (name of the bank), a loan agreement No. 3456272 dated April 12, 2020 was drawn up on the following terms: amount - 500 thousand rubles for the period until March 2020, rate - 18% per annum, intended use - for any purpose.

Since June 10, 2020, my financial situation has deteriorated greatly due to the loss of my job, which is confirmed by the following documents (list of documents that must be attached to the application).

During the entire period of contract No. 3456272 dated April 12, 2015, I made all payments on time and on schedule. There are currently no overdue debts.

Based on the above, I ask you to restructure the debt under my loan agreement No. 3456272 dated April 12, 2015, namely to extend the period for repayment of the principal debt (provide credit holidays, reduce the interest rate) for 1 year, changing the date of full repayment from March 20, 2020 , as of March 20, 2020.

To prepare an application to the bank, you can also use the sample presented below:

Debt Restructuring Law

By law, restructuring can be used for any type of loans, ranging from consumer loans, car loans and ending with mortgage lending.

However, it is important to understand that debt restructuring is not always beneficial to the client. This is the best way out of a situation when there is no loan debt yet. If restructuring is used by the bank as the last step before filing a lawsuit to collect debt from the borrower, you should not rush to agree to the restructuring proposal, since in this case pennies will be included in the amount of the new debt. The court will approve the amount of the debt, but may oblige the bank to write off any accrued fines.

Agreement on debt restructuring between legal entities

In cases where a legal entity (individual) is unable to fulfill debt obligations, the creditor may carry out a special procedure. Its essence is changing the terms of the contract - extending the terms, reducing the percentage or writing off a fine.

This procedure is confirmed by a special document - an agreement on debt restructuring between legal entities.

A standard form of agreement has been developed by many organizations, including the Government of the Russian Federation (for agricultural producers).

Concept of restructuring

The etymology of the word allows us to understand its meaning. The prefix “re” means a repeated, renewable action. Structure – structure, structure. That is, re-building or changing something that already exists. In specialized dictionaries, the term “restructuring” is defined as follows – a change in these conditions (agreement, agreement, contract).

Debt restructuring is a reform of lending conditions based on the replacement of one debt obligation with another, with different servicing and repayment (with optimal conditions for the debtor). Relief occurs by:

- refinancing with more favorable conditions (terms, interest);

- providing “vacations” (the borrower temporarily does not pay the principal debt, only the interest on it);

- currency replacement;

- forgiveness of part of the debt;

- suspension of payment of all kinds of penalties;

- increasing the debt repayment period.

A restructuring agreement (agreement) is a legal document, a civil transaction between the borrower and the lender. The contract specifies all amended terms and conditions of the contract. The document requires the consent of the creditor.

Restructuring allows the debtor to receive more favorable conditions for the return of funds

Examples of a restructuring agreement:

- between the bank and the lender (car loan, targeted loan, mortgage, other credit products);

- between housing and communal services and the owner of the apartment.

In the first option (banking institution), the basis of the agreement is the existing loan agreement. In the case of housing and communal debt, this is a new agreement that stipulates the debtor’s obligations to regularly pay not only for current services (heat, electricity, water), but also for part of the accumulated debt.

Purposes and reasons for use

Despite the terminology “debt restructuring,” the procedure can be started before the debt arises. Reasons leading to changes in debt obligations:

- loss or significant decrease in income;

- the appearance of a dependent (maternity leave, guardianship of children or parents);

- death of one of the co-borrowers;

- receiving disability with physical inability to work;

- conscription;

- currency crisis (ruble devaluation).

The form of restructuring (debt forgiveness, installment plans, credit “holidays”) depends on these factors. Moreover, the agreement may include several forms that are provided to the debtor either sequentially or in parallel. For example, a loan mortgage can be restructured in several stages:

- currency change;

- "holidays";

- refinancing.

As a rule, people with difficult financial situations need restructuring

It is important to understand that the bank’s goal is not “to do better for the client,” but to repay the debt. A financial institution will not simply change the terms of the agreement. Only after documentary confirmation that the client is really unable to pay monthly payments for some reason can the bank “accommodate the meeting.”

In a situation where restructuring is required for a legal entity, the company and the creditor pursue the same goals. It is important for the first party to ease loan obligations, and for the second party to return the borrowed money.

The reasons for a legal entity will be slightly different:

- an initially incorrect analysis of the company’s financial position;

- financial problems that have arisen in the company's activities.

In any case (legal or individual), the restructuring agreement will require the consent of the lender and written confirmation of the borrower's difficulties.

Compilation rules

Any party can initiate the agreement, since the agreement is beneficial to both the debtor and the creditor. A court order to enforce a debt does not guarantee its payment. But most often it is the borrower who takes the initiative.

The order of compilation is as follows:

- The debtor sends an application with a request to change the current terms of the contract.

- The application must be accompanied by copies of documents confirming financial difficulties.

- Obtain the consent of the other party.

- Drawing up a preliminary agreement that stipulates the conditions.

- Verify and sign the agreement.

Documentation must be drawn up in accordance with general rules

The application does not have any specific form. There are general requirements for it, as for any official letter. The application must contain:

- “header” with contact information of the addressee and the applicant (full name, status, address, telephone);

- the word “statement” (in the middle of the sheet);

- the application itself indicates the request to change the conditions, the amount of debt, the reasons for financial difficulties, possible restructuring options;

- date, signature.

In most cases, the contacts of the addressee are the address of the head office of the creditor organization. The application is handed over either to the employee or sent by registered mail with mandatory notification.

If the initiator is a creditor, then, within the framework of the claims made, he sends to the debtor a proposal to restructure the debt on such and such conditions.

The requirements for any agreement are the same: be it a bank loan from an individual, a rent debt or accounts receivable:

- compiled in writing according to a developed model (each institution may have its own form);

- signed only by authorized persons;

- certified by the signatures of the parties (and seals in the case of legal entities).

A mandatory condition for accounts receivable is the provision of a completed agreement with certified signatures to the territorial commission (within 1 month).

It is important to note that the restructuring agreement is not a novelty as the manner of execution does not change. The original contract continues to apply, only some of its terms change.

If documents are completed incorrectly, restructuring may be denied

agreements

The contract must contain the following mandatory clauses:

- personal data of both parties;

- the name of the document that serves as the basis for the debt (loan, mortgage, personal utility bill);

- date of drawing up the contract;

- amount of debt;

- payment extension terms;

- repayment schedule;

- description of the terms of restructuring.

The agreement must be accompanied by a certificate stating the reasons for insolvency.

If the utility debt is restructured, the debtor also documents the crisis situation. In this case, the agreement provides:

- deferment for debt collection;

- additional time to raise funds.

It also exempts you from paying penalties and fines.

Sample agreement

The restructuring process is carried out both between individuals and between legal entities. Debt can arise to various organizations: a bank, housing and communal services, etc.

Accordingly, the content of the agreement will differ. As an example of filling out, you can use various samples of a debt restructuring agreement that are relevant for 2018-19.

For individuals, the most acceptable option is installments.

An agreement to change debt obligations between legal entities has a more complex form. A standard debt restructuring agreement developed by the Government of the Russian Federation can be viewed on the ConsultantPlus website. A sample debt restructuring schedule developed as an annex to the government agreement can be found there.

Thanks to debt restructuring, you can keep your business afloat

Consequences of restructuring for both parties

For the debtor, the entry into force of the agreement means the following:

- the accrual of interest, penalties and fines is suspended;

- For already accrued fines, installments are provided (from 1 month to 5 years);

- refinancing on other terms (terms, interest);

- preservation of business reputation (in case of debt repayment, there is no need to go through legal proceedings with the creditor and bankruptcy proceedings).

It is important to understand that debt restructuring is not forgiveness, but only a deferment of payments. Often, an increase in loan terms increases financial costs.

The credit institution solves the following tasks in its favor:

- the borrower acknowledges the debt (this is important for possible subsequent legal proceedings);

- the period of claim is extended;

- inclusion of clauses favorable to the bank in the amended terms;

- return of borrowed funds (even with partial repayment of interest).

Source: https://gphml5.com/soglashenie-o-restrukturizatsii-zadolzhennosti-mezhdu-yuridicheskimi-litsami/

Application for debt restructuring

A timely written application for loan restructuring is an opportunity to get out of a difficult financial situation with honor without violating your obligations to the bank. Restructuring (carried out in a timely manner) will save your credit history from negativity, and you from additional fines, penalties, and proceedings with the bank.

Remember that it is advisable to write an application for debt restructuring before the first delay on the loan. Firstly, banks are more loyal to conscientious borrowers, and secondly, any late fees will be included in the principal debt during restructuring.

Good afternoon. I would like to tell you about the situation that my dad faced. My dad is a client of Sberbank and has two loans (car loan and cash loan). The family's income has now decreased, so they decided to apply for a cash loan restructuring. I myself am an employee of another Bank and I know that any Bank must accept an application for restructuring due to a reduction in income and consider it either positively or negatively. So this is what we are faced with.

1st request: I don’t specify the date, but somewhere around April 13, 14. The central office is located at Orekhovo-Zuevo st. K. Libnekhta, 4. Dad arrived with a 2-NDFL certificate, which indicated an income of 24,000 rubles, and the monthly loan payment was the same amount. In general, he ended up with a girl, unfortunately, he did not write down the employee’s name and surname. He explains the situation to her, that her income has decreased anyway, and she needs to restructure the loan. To which the employee answers him, but we cannot submit an application, since you are not overdue. When you have 30 days of delay, come and we will accept the application! And she offered to pay at least half of the amount so that the delay would begin. When my dad told me this about what the employee told him, my hair stood on end. Forgive me, but what kind of delay of 30 days are we talking about??? Why should he be late and only then submit an application and ruin his credit history? As an employee of another bank, I know that this is complete nonsense . I decided to call the Bank’s call center. Where three different employees told me that there was no need to allow any delay.

2nd message: 04/21/2015 we are going again to this “glorious department”. The time of our arrival at the department is 17.50. The department itself is, as it were, divided into two parts, one of which provides full service to individuals. We needed to get into another part behind iron doors and with guards at the post. We dial the extension number that the security gives us. After a minute or two, a young man finally picks up the phone, who didn’t even consider it necessary to introduce himself. I stand nearby and listen to the dialogue: - Hello, I need to go to the restructuring department, - answer the phone in the morning (taking into account the fact that clients must be received until 18.00). To which dad replies: I can’t come in the morning because I’m at work at that time. Only then did the young man decide to inquire about why we were restructuring, to which they answered that income had decreased. And again we hear in response that we do restructuring only after 30 days of delay. And the phone was hung up...

Explain to me, please, what kind of mockery is this? And where are the bank employees’ ethics for communicating on the phone??? On this, of course, we decided not to give up. We go into the hall where FL is being serviced, approach the girl, I can’t tell her name, since the employee did not have a badge with her name and surname. She also didn't introduce herself. As I understand it, the employees of this department, in principle, do not consider it necessary to introduce themselves??? She asked to call the manager. In response, why? I explain the whole situation to her. An employee tells me that the manager is in the other wing. I answer, call me the manager!!! The girl starts calling somewhere and then returns and tells me the following: “Yes, indeed, the employees cannot accept the application, since they have issued an internal order that the restructuring will be done after 30 days of delay.” I ask her to show this order and she answers that it is necessary, what is there, to write something and register it somewhere. Ok, I think and ask her to give us a form to write a complaint and what do you think she answers me? Write on a piece of paper and go register with the secretary... What??? Which secretary??? Does Sberbank lack a book of reviews and suggestions or a general claim form??? In general, once again I leave this department in complete shock...

We leave the branch, and I once again call the call center, where I again explain the whole situation, to which they again tell me for the 4th time that there is NO NEED TO COMMIT ANY DELAYS! A complaint was left with an employee over the phone. Another question arises: do branch employees and call center employees have different information??? Or maybe managers simply don’t consider it necessary to bother with restructuring? Just because I am an employee of another bank and know how applications for restructuring are accepted, I decided not to just leave it and write complaints and leave claims. What should people do who have not encountered such situations? Commit delays and ruin your credit history? Again, I conclude from this that the Bank is pushing its clients to overdue!!! Is it normal?

Please be so kind as to help me understand this situation. Even if this order supposedly exists. We need a written refusal from the bank to provide restructuring, because in the event of a lawsuit, we will be able to provide it. And they don’t even let us write a statement and kick us from one corner to another.

Bank debt restructuring

Restructuring, unlike refinancing, can be processed exclusively at the bank where the loan was issued.

In fact, both of these phenomena are similar and are aimed at creating more favorable, loyal conditions for loan repayments for the borrower. Only in the case of refinancing, you take out a loan from another bank on more favorable terms, while restructuring involves working with the bank from which you took out the loan: you may be offered a “credit holiday,” transfer of debt from one currency to another, or an increase in the term lending with a corresponding reduction in interest.

Loan debt restructuring: what is it?

Loan debt restructuring is a set of bank measures aimed at easing the loan burden for the borrower. Debt restructuring is usually resorted to in cases where the borrower’s financial situation has changed so much that he cannot pay the amounts required by the original loan agreement.

Not all banks are willing to restructure the debt, and some offer not very favorable restructuring conditions. Therefore, if you are planning to take out a large loan from a bank for a long time, ask on what conditions and in what cases the bank you have chosen will be ready to carry out restructuring.