Most banks and credit institutions today have fairly strict requirements for borrowers. This precaution is mainly associated with an increase in delinquencies under loan agreements and the unpleasant statistics of bankruptcy of not only legal entities, but also individuals. Often, the lender insists on a guarantee - the assumption by a third party of responsibilities to guarantee the timely payment of payments by the borrower. However, today many Russians are wondering how to terminate a guarantee agreement if the main borrower is declared insolvent.

Liability of the guarantor in bankruptcy

Thus, the legislation of the Russian Federation does not establish requirements for the level of wages, the availability of property, or the financial condition of the person acting as the guarantor. These issues remain at the discretion of the parties to the loan agreement. In this regard, we note that in accordance with Article 216 of the Federal Law of October 26, 2002 N 127-FZ “On Insolvency (Bankruptcy)” (hereinafter referred to as the Insolvency Law), from the moment the arbitration court makes a decision to declare an individual entrepreneur bankrupt and on the opening of bankruptcy proceedings, the state registration of a citizen as an individual entrepreneur becomes invalid.

How does the bankruptcy procedure for individuals proceed with guarantors?

In essence, the bankruptcy of the guarantor of a legal entity or individual. the face does not have any special features, the procedure takes place as usual. Let's look at how this works.

- An application for bankruptcy of the guarantor is drawn up. The document indicates the amount of debt, creditors, the reasons that prompted you to file for bankruptcy, as well as the SRO from which the financial manager will be selected.

- Documents are collected and attached to the application. In particular, claims, claims from banks, documents on the applicant’s marital status and a number of others.

- All receipts are paid and attached. In particular, 25 thousand rubles are deposited, this is a reward for the financial manager. The state duty is paid - from January 2020 its amount was 300 rubles.

- A procedure is prescribed. Practice shows that in most cases the courts order the sale of property. Also, if the appropriate decision is made, the bankruptcy of the guarantor-individual is recognized.

- The arbitration manager carries out all the necessary procedures, after which he draws up a report for the court. The remaining debts are written off.

Termination of guarantee in case of bankruptcy of the debtor

In my opinion, the guarantor continues to be jointly and severally liable.

According to Art. 142 of the Zoba, the creditor’s claims are considered extinguished, but not satisfied. In this connection, creditors have the opportunity to satisfy them in other ways provided by law, including collection from the joint debtor.

The Zob, strictly speaking, is silent about this situation as such, so we apply everything according to the Civil Code about joint and several liability.

Alexey Vladimirovich, according to Article 367 of the Civil Code of the Russian Federation, the guarantee is terminated.

When a bankruptcy procedure is initiated against a borrower, the guarantors have a reasonable question: “what will happen to their property?”, because they are also responsible for the obligations of the debtor who is in bankruptcy. However, upon completion of bankruptcy, the debts of creditors to the debtor are subject to write-off by operation of law.

We recommend reading: Procedure for registering a garage as your property

At first glance, the situation is contradictory, because when writing off the principal debt on a loan (credit), i.e.

Article 367 of the Civil Code of the Russian Federation on termination of a guarantee - grounds for termination of a guarantee

It is imperative that both the creditor and the debtor give consent to carry out such an operation.

- Upon expiration of the period specified in the contract.

- Upon termination of the secured obligation;

- Transfer of all obligations to a third party (for this method it is important that the new guarantor also agrees to be responsible for the debtor);

- If the creditor refuses to receive the proper performance specified in the agreement;

- If the obligations have been changed without confirmation from the guarantor. This often entails more responsibility for the individual. Therefore, if such actions were carried out without his consent, he continues to be liable for previously established obligations;

Under Article 367 of the basic civil law, banks very often go to court.

When does the guarantee end?

According to the Civil Code of the Russian Federation, there are four grounds when a guarantee may end:

If the guarantee period has expired. This may be the end of authority under the contract or early if the debtor has repaid the loan.- If the creditor refuses to accept this type of performance.

- Termination of guarantee in case of bankruptcy of the financial debtor. However, this only happens if the borrower is officially declared bankrupt and the creditor has filed a claim against him in court. Moreover, this must be included in the bankruptcy register. Only in this case is the guarantor relieved of the obligation to bear responsibility for the borrower.

Some people don't know, but the death of the debtor does not terminate the guarantee. This liability can be terminated if the guarantor has stipulated in advance the fact that in the event of the death of the debtor he will not be responsible for his heirs. If this nuance was not specified, then the guarantee continues. Another possible option for stopping this activity could be the lack of inherited property.

Responsibility of the guarantor in case of bankruptcy of the main borrower

Before becoming a guarantor in a borrower’s loan agreement, it is worth knowing that the legislative norms stipulate that in the event of bankruptcy of the main borrower, the guarantor undertakes to be liable for the bankrupt’s obligations.

If a creditor brings a claim against both the debtor and the guarantor, he must take into account the size of the claims. If the creditor's claims have already been established in the bankruptcy case of the main debtor, then in this case the composition and amount of claims against the guarantor are determined based on the date of introduction of the bankruptcy procedure in relation to the main debtor.

A guarantee is one of the common ways to secure a loan agreement, leasing, government contract and other obligations.

We recommend reading: Documents for renouncing Russian citizenship

Under a guarantee agreement, the guarantor undertakes to be responsible to the creditor of another person for the latter’s fulfillment of the obligation in whole or in part. A surety agreement is always concluded in writing. The guarantee agreement always specifies the basic conditions of the secured obligation, the size, limits and period of liability of the guarantor.

Features of the bankruptcy procedure of a guarantor for a legal entity

If another legal entity becomes the guarantor of a legal entity, then it has the right to declare itself bankrupt, but the conditions of bankruptcy will be different. Thus, a legal entity can declare its insolvency if the total amount of debt exceeds 300 thousand rubles, and the duration of the delay is 3 months.

Bankruptcy of a legal entity-guarantor involves going through the following stages of bankruptcy:

- Submitting an application to declare the company financially insolvent to the arbitration court.

- If the application is found to be justified, the court introduces an observation stage and appoints a temporary manager.

- A register of creditors' claims is formed and the first meeting of creditors is held.

- At the request of creditors, the court introduces one of the rehabilitative stages of bankruptcy of a legal entity : external administration or financial recovery.

- If at these stages it is possible to fully pay off your obligations, then the bankruptcy procedure is terminated..

- In cases where it is impossible to repay one’s debts under a surety agreement, the court enters the stage of bankruptcy proceedings against the legal entity.

- At the stage of bankruptcy proceedings, a bankruptcy estate is formed from all the debtor’s property, which is then sold at auction . It includes fixed assets, vehicles, real estate, accounts receivable, etc.

- The proceeds are used to pay off creditors' claims, taking into account the priority established by law . The claims of creditors under the guarantee agreement are repaid as part of the third priority, together with obligations for mandatory payments.

- Upon completion of settlements with creditors, the company is liquidated.

If the guarantor for the obligations of a legal entity had the status of an individual, then he goes bankrupt like an ordinary citizen under the provisions of Chapter 10 127-FZ.

For guarantors of a legal entity, it should be taken into account that they will not be able to declare themselves bankrupt for debts associated with their being brought to subsidiary liability as part of the process of declaring the company financially insolvent. Only a court has the right to hold the manager, owner and employee of an enterprise liable for subsidiary liability, and only after or during the enterprise’s bankruptcy procedure.

Bringing to vicarious liability means that management is to blame for the financial collapse of the company.

What is bankruptcy?

Before understanding the role of a guarantee, you should study the nuances of a possible bankruptcy of an enterprise. Even if the company for which you were offered to guarantee is far from being threatened with bankruptcy, you should prepare in advance for a negative scenario, because anything can happen - for example, a crisis can lead to bankruptcy.

Generally,

bankruptcy today refers to the loss of an enterprise's ability to fulfill its obligations to creditors and other persons. In other words, the company assumed a number of obligations, but at some point experienced financial instability and came to complete insolvency. On the one hand, bankruptcy means losses and other financial losses, debts and just a headache.

On the other hand, bankruptcy is in some cases the only way out of difficult situations and truly saves enterprises from complete collapse. A competent bankruptcy procedure allows you to leave the market almost painlessly, while part of the company’s debts can be written off.

Bankruptcy can be different. The worst version of bankruptcy is a complete collapse, in which the company cannot pay off its own debts at all and is forced to repay debts to creditors for a long time, pay salaries, etc. A completely different bankruptcy is technical, when in general the company almost completely copes with its debts, but still a little can't cope with problems. In this case, the company may be officially declared bankrupt, but in reality the company pays all debts late and returns to the market.

You may also be interested in:

- What are the risks of bankruptcy of a developer and what to do if the developer is bankrupt?

- Intentional or fictitious bankruptcy, main signs and punishment

- What will happen to employees if the company goes bankrupt?

The procedure for bankruptcy of a guarantor of an individual or legal entity for a loan

Reading time: 5 minutes(s)

From a legal point of view, a guarantee is one of the ways to ensure and guarantee the fulfillment of debt obligations to the creditor. But since, in connection with the recently adopted law, ordinary citizens can now accept bankruptcy status, many potential guarantors and creditors need to know what the bankruptcy of a guarantor of an individual and legal entity for a loan can lead to.

How bankruptcy of a guarantor of an individual or legal entity for a loan is carried out

Responsibility of the guarantor and consequences in case of bankruptcy of the borrower

The meaning of a guarantee is that if certain circumstances arise, it is not the borrower, but the guarantor, who will repay the debt to the creditor. For financial institutions, it makes no fundamental difference who repays the loan - the most important thing is that the funds are repaid in full and on time.

The obligations of the guarantor may not be present at the time of concluding the contract, but will appear after some time.

In other words, the guarantor’s duty is to come to the aid of the borrower if he has problems fulfilling his loan obligations, and to make loan payments for him.

The guarantor and the borrower are jointly and severally liable to the lender, unless the contrary was stated in the agreement.

Since the bankruptcy of the borrower terminates all of his debt obligations, the obligations of the guarantor must also be completed. However:

If during the bankruptcy stage of the proceedings the debtor’s personal property was not enough to fully repay the debt to the creditor, then according to clause 9. Art. 142 of the Insolvency Law, the debt will be considered extinguished.

Based on clause 11 of Art. 142 financial organizations have the opportunity to receive the missing amount, and on the basis of Part 1 of Article 367 of the Civil Code, the appeal will not terminate the guarantee even if the debtor is liquidated.

Thus, the organization has the right to fulfill its obligations in full even after completion of the bankruptcy procedure and liquidation of the debtor.

It is important to understand that bankruptcy implies a situation in which the guarantor fulfills the obligations of the debtor, but not vice versa.

And for the borrower, this means that the option through which it would be possible to fulfill his obligations to the lender will disappear.

As a rule, in such a situation, the debt is repaid before the date specified in the contract. And on the basis of Article 62 of the Arbitration Procedure Code, the debtor will be involved in the case if his guarantor accepts bankruptcy status.

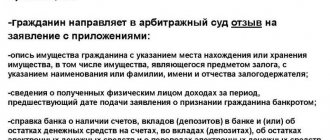

Bankruptcy of a guarantor is a procedure carried out under the general conditions for recognizing the financial insolvency of an individual - to begin the process, it is necessary to provide the court with an application from the citizen and a package of documentation for consideration.

Based on the results of the consideration, the arbitration court will decide on debt restructuring or the sale of the debtor’s property. Sometimes the case is resolved by concluding a settlement agreement between the parties, approved by arbitration.

As practice shows, in most cases a restructuring process is used, which is carried out according to a plan approved by the court. The commencement of the bankruptcy process will temporarily suspend enforcement proceedings regarding the collection of loan debt.

During debt restructuring, the guarantor pays off his own debts. In case of full repayment of the remaining amount of the debt, the guarantor has the right to demand the amount repaid by him from the borrower.

If the bankruptcy process has also been launched in relation to the borrower, then, subject to certain circumstances and compliance with the procedure and deadlines, the guarantor may be included in the register of creditors in this financial insolvency case.

If the arbitration has made a decision to sell the property of the guarantor-debtor, or the restructuring procedure has not yielded positive results, then the financial manager begins to evaluate and sell the debtor’s personal property. The funds received will be used to pay off debt claims according to the order of priority. Unpaid claims will be canceled, and if after fulfillment of all obligations there are still available funds, they will be transferred to the guarantor.

The guarantor retains the right to demand repayment of the debt to the borrower, unless the latter was declared bankrupt for some reason, while the guarantor paid the entire amount of the loan in his place.

This right of claim can be exercised during the legal process; for this, the guarantor needs to receive a writ of execution, on the basis of which the bailiffs will begin the forced collection of funds paid by the guarantor.

In addition, it can also be implemented by filing an application to declare the borrower bankrupt if the amount of debt does not exceed 500 thousand rubles , and the debtor is overdue for repayment of the loan by more than 3 months.

Features of a guarantor's bankruptcy

Termination of all obligations of the debtor due to its liquidation means a change in the main obligation, entailing adverse consequences for the guarantor. Such consequences include the occurrence of circumstances in which the guarantor is deprived of the opportunity, in the event of fulfillment of the borrower’s debt obligations, to receive reimbursement from him for expenses incurred.

According to paragraph 1 of Art. 367 of the Civil Code, such changes are grounds for termination of the guarantee.

Some banking institutions insist on including in the loan agreement a condition that in the event of bankruptcy of the borrower, the guarantor remains obligated to answer for this debt obligation. It is important to understand here that this condition has no legal force and does not entail any legal consequences, since it is contrary to the law.

Thus, the liquidation of the debtor means the termination of the obligations of the guarantor, regardless of whether the borrower is an individual or a legal entity.

Grounds for refusal

The grounds for refusing bankruptcy for a guarantor are the same as for ordinary citizens:

- outstanding convictions for crimes of an economic nature or damage to property;

- fictitious or deliberate bankruptcy;

- repeated application for bankruptcy status in the previous five years.

Is it possible for a guarantor to go bankrupt without a court decision?

It is impossible to file bankruptcy of a guarantor of an individual without a trial, since the federal law on the insolvency of individuals provides for a certain algorithm of actions for accepting bankruptcy, based on close cooperation with the Arbitration Court.

How does the procedure work?

The bankruptcy of the guarantor begins, first of all, with the declaration of bankruptcy of the debtor. If the borrower himself accepted the status of bankrupt, then in the process of filing financial insolvency, the court deprived him of his personal property, leaving only an apartment and basic necessities.

Attention: Even if, from a legal point of view, the loan is “liquidated”, this does not mean that the guarantor is exempt from paying it. If the debtor’s personal funds are not sufficient to fully repay the debt, then the creditor has the right to sue the guarantor in court demanding payment of the balance.

Since debt obligations concern not only the borrower and the guarantor, but also the creditor, after the borrower accepts bankruptcy status, the organization transfers all the necessary documentation and rights to the guarantor.

In this case, the guarantor also has the right to file a claim in court to declare himself bankrupt. The same set of measures will be taken against him as were applied to the main debtor. In this case, the decisive circumstance is the date of fulfillment of the guarantor’s obligations to the bank.

If the guarantor fulfilled his obligations before the borrower was declared bankrupt, then he can use the reverse right.

Such a claim will protect the guarantor from disappearing from the borrower’s sight, and will also bind the debtor and the guarantor jointly and severally liable. In other words, the creditor will not demand payment on the loan until the debtor himself is declared bankrupt. Otherwise, if the debtor’s funds were not sufficient to repay the loan, the organization will oblige the guarantor to pay only the remaining amount.

If the loan was repaid by the guarantor before the borrower was declared bankrupt, then the guarantor has the right to become a bankruptcy creditor and demand reimbursement of expenses incurred from the debtor.

Thus, the blame for non-payment of debt lies entirely with the borrower himself, since:

- during the initiation of bankruptcy proceedings for the guarantor, the court takes into account its status as a regressive claim, as a result of which the guarantor may become a bankruptcy creditor;

- if the court has grounds to believe that the claims can be satisfied at the expense of receivables, then the application for bankruptcy status will be rejected at the stage of its filing.

As a result, banking institutions initiate the process of filing bankruptcy first of all with the borrower, and only then with the guarantor. As a rule, guarantors decide on the need for bankruptcy only after a court decision against the borrower.

Attention: To obtain bankruptcy status, the guarantor must meet the same requirements as the borrower.

If an application for bankruptcy status was filed with the court after the main borrower was declared bankrupt, then the process of consideration of the case takes place under the same conditions as if the guarantor was a debtor.

According to the law, when confirming the bankruptcy status of any individual, including a guarantor, the following occurs:

- debt restructuring;

- inventory of personal property, accounts and amounts on them;

- sale of property;

- if the proceeds from the auction are not enough - repayment of the balances;

- release of the guarantor from credit debt.

The bankruptcy of a guarantor does not present any difficulty, since it is carried out according to the general rules of financial insolvency of citizens. However, due to the short duration of legal provisions and possible difficulties associated with the factual circumstances of the case, developments may be difficult. Each specific case requires a careful approach and comprehensive analysis, taking into account all the circumstances and features, so you should not look for a universal solution.

Did this article help you? We would be grateful for your rating:

0 0

Collection of debt from the guarantor after the main debtor has been declared bankrupt.

What will happen to the guarantor if the debtor goes bankrupt? What will happen to the guarantor if the bank demands to repay the debt for the main debtor who does not pay the loan? If cancellation fails, there are two options left: pay the debt or declare yourself bankrupt. In the first case, after repaying the debt to the bank, the guarantor can contact the debtor and demand reimbursement of expenses.

The parties can sign an agreement or resolve the dispute in court. If the procedure for recognizing the financial insolvency of the borrower has been launched, the guarantor can participate in the case as one of the creditors. Declaring bankruptcy can help get rid of debts, but you need to consider the consequences of this procedure, including the fact that the guarantor's property will be seized and sold to pay off the debt.

Can a guarantor be declared bankrupt because of a borrower?

366 of the Civil Code of the Russian Federation, the debtor is obliged to notify the surety; if the debtor fulfilled the obligations but did not inform the guarantor, and at the same time the guarantor also fulfilled these obligations, then the latter has the right to present a recourse claim to both the debtor and the creditor. 32.

- a person in relation to whom bankruptcy was carried out will not be able to go through the procedure again within a 5-year period after the completion of the sale of property and for 8 years after the completion of debt restructuring;

- a bankrupt person will not be able to hold leadership positions for 3 years. Thus, you will temporarily not be able to be the general director or be on the board of directors of the organization;

- within 5 years you will not be able to open an individual entrepreneur;

- the bankrupt will not be able to hide the fact of bankruptcy and take on new loan obligations without prior notice to the credit institution;

- your credit history will be ruined.

Consequences of bankruptcy of individuals: what awaits the bankrupt and his relatives

- inability to donate assets or contribute them to the authorized capital of the LLC;

- restriction on traveling abroad (if such a decision is made by the court);

- inability to use property as collateral;

- any actions to register or re-register property can be carried out exclusively by the financial manager;

- bank accounts, deposits, cards are transferred to the manager;

- transactions for the acquisition of property for a lump sum of more than 30,000 rubles as part of debt restructuring are carried out by the borrower only with the knowledge of the manager, as part of the sale - exclusively by the manager;

- inability to carry out transactions for the purchase and sale of shares in the capital of legal entities and shares;

- You cannot act as a guarantor, guarantor, or purchase and sell debts.

We recommend reading: Calculation of tax from cadastral value