May 23, 2020 3756

- >

- Credit lawyer services…

- Disputes with collectors: recognition...

>

Legal services for invalidating assignment concluded by banks and debt collectors , preparing counterclaims against debt collectors, drafting responses to claims by debt collection organizations in Novosibirsk. Representation of borrowers in court regarding claims by collection organizations. Reducing the amount of debt, debt.

In practice, the following situation often arises. The borrower entered into a loan agreement with the bank and made late payments on the loan. It was not the bank, but the collection agency(ies) that filed the lawsuit against him.

This happens when the bank has assigned its rights (claims) under the loan agreement to a non-bank organization (collection agency).

If the borrower did not give his consent to the assignment of rights of claim in favor of an organization that does not have a banking license, then in court, under certain circumstances, it is possible to invalidate the agreement on the assignment of rights (claims).

In addition, the amount of debt calculated by the collection agency can be challenged in court on other grounds.

What to do if collectors bought the debt from the bank?

Due to the fact that your debt was collected in court by the bank, there was enforcement proceedings, the bank could sell the debt only under an assignment agreement (assignment of rights).

In this case, you must be notified by a court summons, sent you a statement, and this assignment agreement (assignment of rights) between the bank and the collection agency must be enclosed as attachments.

We answer! Our website contains the most exciting, most pressing questions that Internet users ask on the Internet. We tried to give a comprehensive answer to each question. You can comment on the answers or ask your own question.

Collectors buy the debt at a reduced value and begin to demand the return of the entire amount with accrued interest, which was calculated solely at their personal discretion. In this case, calls, conversations, personal visits, threats and other unpleasant methods begin. Should I pay the collectors? The debtor is not obliged to do this, much less pay the entire required amount. For your debt, the bank is forced to create a reserve of money in an amount 2 times greater than your debt. This greatly pollutes the bank's balance sheet.

Formally, it will have to act as the acquirer of the debt, that is, a party to the assignment agreement. Direct transactions with debtors are risky. Despite the absence of a direct prohibition in the laws, they lack specifics.

But now the borrower needs to be even more careful when concluding a loan agreement, lawyers say.

By the verdict of the Oktyabrsky District Court of Samara, the Principal was found guilty of committing crimes under Part 3 of Art. 30, paragraph "d" part.

By the way, I have in my arsenal such a service as accompaniment to the bank for an assignment transaction. If necessary, please contact us!

After 3 years, the writ of execution was no longer sent to the bailiffs. Then a notification was received from the bank about the need to pay personal income tax on the income generated as a result of writing off the debt.

Sometimes in practice, collectors indicate in a letter their details for paying the debt. However, we recommend that in this case you pay the loan debt directly to the bank in order to avoid controversial situations and misunderstandings. If the letter is called a “notice of assignment of claims,” we are talking about the second option. Law office "Antonov and Partners" - high-quality legal assistance throughout Russia. Your region doesn't matter!

Today, the most effective method of countering debt collectors who go to court is to challenge the assignment agreement on the basis of: Didn’t find the answer to your question?

Unfortunately, you can’t just come to the bank and say: sell me the debt! You need to wait until the bank generates a personal offer for you. You can find out about it by calling the bank's hotline.

Banks often sell overdue debts in bulk to collection agencies. It may happen like this. that the financial institution has accumulated a huge base of overdue debts, and it wants to get rid of it quickly.

What does the recognition of an assignment agreement as invalid give the debtor? Formally, again, nothing changes - the debt remains the same. Just goes back to the bank. But in reality, the situation looks quite interesting: the collector no longer has the right to demand repayment of the debt, and the bank has already written off this debt.

Therefore, when the bank understands that there is no longer a chance to return the money lent to the borrower, the financial institution assigns the claims to another person. This process is called assignment, and the person to whom the debt is transferred is called the assignee.

What does the recognition of an assignment agreement as invalid give the debtor? Formally, again, nothing changes - the debt remains the same. Just goes back to the bank. But in reality, the situation looks quite interesting: the collector no longer has the right to demand repayment of the debt, and the bank has already written off this debt.

According to what is described in it, the creditor actually has the right to transfer the debt to another person under an assignment agreement concluded with him. The debtor's consent to this action is not required unless otherwise provided in the loan agreement between the bank and the borrower.

Collection offices do not work according to the law, since there is an agreement between the bank and the borrower, where the latter must repay the borrowed amount with accrued interest. When the bank has sold all the debt to a collection agency, its employees begin active efforts to “knock out” the debt.

Assignment agreement. But here a completely different scheme works. The bank actually sells the debt of the “negligent” borrower to the collector, and he, in turn, becomes his new creditor.

Find out whether to pay collectors money under an assignment agreement. Here you will find expert answers on whether it is worth paying debt collectors for overdue loans, and whether the bank has the right to sell the debt to debt collectors.

Legally, there are no obstacles to such a transaction. Therefore, the debtor always has the opportunity to negotiate with collectors about the next repurchase of his debt. How much can you buy it for? The amount of debt repayment in each individual case is individual and will depend on a large number of different factors: financial, economic, legal, etc.

At what stages is the cession concluded?

The conclusion of an assignment agreement is possible at different stages:

- pre-trial;

- judicial;

- in the process of enforcement proceedings.

At the pre-trial stage, the assignor assigns debts without attempting to collect debts through the court. The assignee may also attempt to recover the money directly from the borrower. If this does not produce results, the new creditor has the right to sue.

A change of creditor may occur during the trial stage. Then the plaintiff will be the assignee under the assignment agreement. In this case, they do not start a new trial, but continue the one already started. The same procedure for changing an old creditor to a new one occurs in the process of enforcement proceedings.

Materials on the topic “Mortgage, loans”

That is, if collectors purchased your debt at a price of 1-2% of the amount, then they will demand 10-20% from you.

The essence of the matter is this. The bank, under an assignment agreement, assigned the mortgage debt of its client, Mr. Golovanov, to a third party - Alliance Mortgage OJSC.

We recommend that, as soon as possible after receiving the notification, write a response letter to the collectors, in which you need to ask them to provide you with a duly certified copy of the agreement on the assignment of rights of claim between the bank and the collection agency, as well as documents directly related to your loan (loan agreement, bank statements account, etc.).

In case of unsuccessful pre-trial settlement of the dispute, the case may indeed be referred to the court, but it makes a verdict based on the law. Therefore, the unauthorized accrual of penalties, interest and other unlawful fines by collectors is reduced to zero.

As you know, in Russia almost every fifth loan is overdue. According to the Central Bank, 5–6.5 million compatriots are experiencing difficulties servicing their debts.

Communicating with a collection agency can hardly be called a pleasant experience; the question is how legal is the assignment of claims, whether you are obliged to communicate with collectors, and who to pay the money to.

Even if the “sale” of the debt took place without the participation and consent of the borrower, the latter must be notified at least by registered mail with return receipt requested.

We remind you that any notifications, except for registered letters, are of a formal nature and are not a sufficiently compelling reason for fulfilling financial and credit obligations, especially since there is no need to transfer money to the account of third parties.

Contract form

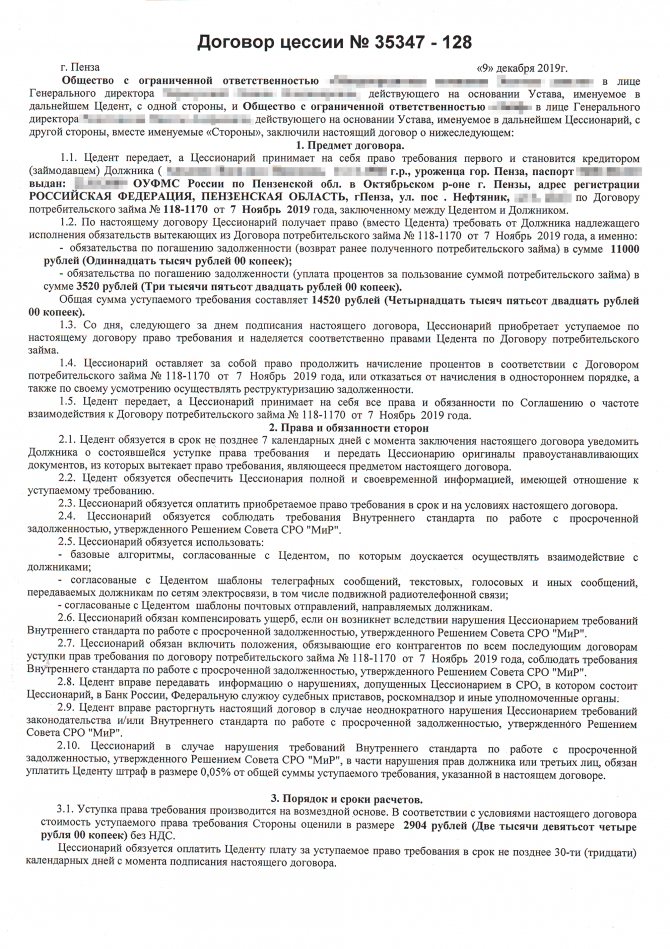

Typically, an assignment agreement consists of the following sections:

- Subject of the agreement.

- Rights and obligations of the parties.

- Responsibility of the parties.

- Procedure and terms of payments.

- Other conditions.

- Requisites.

Sides and subject. The assignment agreement is concluded between the assignor, the assignee, and sometimes the debtor is also involved. The details of all parties must be indicated in the contract without errors. You can check the details of an organization and an individual entrepreneur through an extract from state registers - the Unified State Register of Legal Entities and the Unified State Register of Individual Entrepreneurs.

By the way, it will be written there who has the right to sign documents on behalf of the organization without a power of attorney. Usually this is the leader. If someone else signs, it is worth checking whether their power of attorney has such rights.

We invite you to read: Taxation of payments under a GPC agreement

The subject of the assignment agreement is the transfer of a specific claim from the assignor to the assignee. The requirement must be described in such a way that it can be clearly defined:

- The basis for the requirement and what documents support it. For example, indicate the number and date of the agreement that the assignor concluded with the debtor.

- What does it represent? For a monetary claim, it is necessary to decipher in detail what the debt consists of. If the amount includes interest, penalties, fines and penalties, then it is better to attach a calculation.

- Details of the debtor and assignor.

This is what happens if you don’t specify the requirement in the most detailed way. Mikhail, Sergey and Alexander rented out premises to the bank. At first everything was fine, then the bank stopped paying, and the debt accumulated.

The lessors assigned the right of claim to the bank to another organization. But the debtor was able through the court to recognize the assignment agreement as not concluded.

The court decided that it was impossible to determine the claim from the contents of the assignment agreement: the agreement did not specify what the amount of the debt consisted of. Only penalties are highlighted separately, and everything else is dumped into a common pile. And there are big questions about penalties: the period for their accrual is not even indicated, and there is no calculation.

Also important, but not essential, terms of the contract are:

- Notifying the debtor of the assignment - who does it and when.

- When the assignor receives payment.

- When the assignor transfers to the assignee documents confirming the debt.

- What documents exactly confirm the debt? It is better to provide a list with details.

- At what point does the claim pass to the assignee: at the time of conclusion of the contract, after payment, or at some other time.

- What happens if the debtor suddenly pays the assignor and not the assignee. By default, then the assignor must transfer this money to the assignee, but the contract can and should specify: in what time frame, who, whom and how notifies about the erroneous payment.

- Penalties for violation of obligations and jurisdiction.

- Is the old creditor obliged to help the new one in collecting the debt: provide additional documents upon request, go to court hearings, if necessary.

By law, the assignor is responsible for the invalidity of the claim. That is, if he cedes a dummy - a debt that does not exist - the assignee will be able to demand money back from him. There is a trick here: if the assignment agreement states that the assignor is not responsible for the invalidity of the claim itself, then it will not be possible to recover anything from him. But there are conditions:

- The requirement must be related to business activity.

- The assignor himself did not realize that the claim could be declared invalid, or he knew, but warned the assignee about this in advance.

Sample assignment agreement. Here is a standard agreement. From it you can create something suitable for specific requirements, interests of the parties and the situation. It can be done so that it mainly protects the interests of the assignor or, conversely, the assignee.

The assignment agreement has to be adjusted to different situations and requirements. In this case, the assignor demanded that the assignee agree with him on the text of SMS and letters that he plans to send to the debtor

Lawyer's advice: what to do when the bank sold the debt to collectors?

It turns out that in this case, the debtor, firstly, protected himself from attacks from collectors, and secondly, he did not owe anything else, and he paid, in fact, only part of the total amount.

You will learn further about what to do if the bank sold the debt to collectors, how legal is the transfer of rights to claim debt obligations, and how to behave.

Most often, banks resort to the procedure of selling bad loans in the following cases:

- The borrower does not repay the loan for a long time, and it is not profitable for the bank to collect it due to the small amount of the loan, for example, up to 350 thousand rubles.

- The bank managed to legally oblige the borrower to repay the loan debt, but the bailiffs, for various reasons, are unable to collect the debt.

Typically, the demand letter to the debtor will indicate how the debt collector is related to your debt (the services of an intermediary or a direct sale of the debt). There must be a link to documents, such as an agency agreement or assignment agreement.

Challenging the loan agreement and assignment agreement

As explained by the Supreme Court, the Law on the Protection of Consumer Rights does not give banks and other credit institutions the right to transfer rights of claim under loan agreements with an individual (consumer) to third parties who do not have a license to conduct banking activities. Therefore, the answer to the question whether a bank can sell debt to collectors without a court decision will be positive. How lawfully this was done specifically in your case is another matter.

In cases of departure of one of the parties in a controversial or established legal relationship (death of a citizen, reorganization of a legal entity, assignment of a claim, transfer of debt and other cases of change of persons in obligations), the court allows the replacement of this party by its legal successor. Succession is possible at any stage of civil proceedings.

Refer to the melon text within the framework of Art. 388 won't work. Conclusion The sale of a legal entity's debt to collectors does not violate the law. Debtors need to study their rights in detail and actively defend them.

Features of the application of cession

Assignment is used in different fields of activity, and each has its own specifics. For example, the rules of assignment in lending are specified in Federal Law No. 353-FZ, in shared construction - in Federal Law No. 214-FZ, in bankruptcy - in Federal Law No. 127-FZ.

I will analyze the features of the application of cession in each area so that you do not have to leaf through these boring laws.

The shareholder can be either a person or an organization. For example, a contractor with whom the developer paid with apartments. Or an investor who expects to buy cheap, then sell high and make money. Or an ordinary person buys an apartment to live in or rent out.

The DDU is subject to state registration, which means the assignment agreement will also have to be registered. If you purchase an apartment from an organization under an assignment agreement, you pay after the assignment is registered - this is required by law. If it’s an individual, you can give the money right away, but it’s still better to wait for registration.

If there is no such condition, then the assignor and assignee have the right to formalize the transaction without asking the opinion of the developer. But you will need to notify him of the assignment in writing in any case.

According to the supply agreement. Rights of claim under a supply agreement can also be assigned. For example, an organization delivered products to a buyer, but for some reason did not receive money. Or, conversely, the buyer paid for the goods, but they still didn’t deliver them.

It also happens that a small company wants to supply products to a large chain. The network says: “No problem, we only work on deferred payment terms. We will pay the money 2 months after delivery.” The supplier risks a cash gap if he agrees.

This is more profitable for everyone: the supplier receives payment for the goods immediately, the buyer receives installments, and the factor receives a commission for services.

It must be remembered that the intermediary will not buy out the claim at a loss. If he offers something to the victim, it means he expects to receive much more from the insurance company. You should evaluate how profitable such a deal is and whether they are trying to deceive you.

We invite you to familiarize yourself with: Changes in the essential terms of the contract after execution

The insurance company's obligations to the victim cease upon assignment. Unscrupulous insurers take advantage of this by slipping assignment agreements for signature and transferring the claim to an intermediary. And the victim receives from the intermediary a penny compensation or the most lousy repair.

The main rule of legal literacy applies here: first read, then sign. And if anything is unclear, consult a lawyer first.

It also happens that the assignment is used in anticipation of bankruptcy. The company understands that the situation is bad and is trying to transfer its claims to another legal entity so that they do not go to creditors. Such transactions are contested if they were completed three years before filing a bankruptcy petition or later.

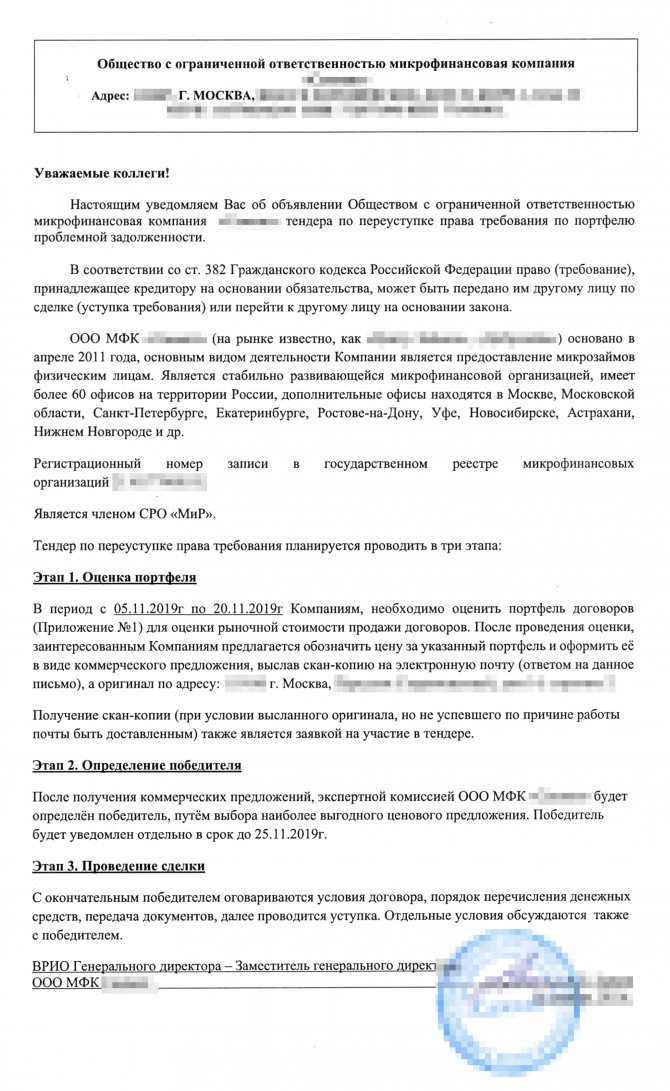

In credit banking operations, everything happens something like this: the lender has a package of debts and a desire to sell it. Then he informs the collectors: “There is a lot of 100 contracts, without collateral or guarantors, almost all of them have court orders or decisions, the total amount of debt is 50 million rubles, the average period of delay is 400 days. Who will give how much {q}.” The one who pays more will take all the claims.

Creditors send such letters to collectors, to which they attach an anonymized list of debts. If the proposal is of interest to the organization, it can offer its price for the portfolio and participate in the tender

Consequences of selling debt to collectors

To do this, we turn to the loan agreement. You need to read it in detail and look for one of the following formulations:

- the lender has the right to fully or partially assign its rights and obligations under the Agreement, as well as under transactions related to securing the repayment of the loan, to another person without the consent of the Borrower.

- the lender has the right, without the consent of the Borrower, to fully or partially assign its rights and obligations under the Agreement, as well as under transactions related to securing the repayment of the loan, to another person who does not have a license to carry out banking operations.

We found out whether banks have the right to sell debts to collectors - this action is not prohibited by law, but who should notify the borrower about this, the bank or the collector? Having sold the obligations of their client, banking organizations, according to the assignment agreement, are obliged to notify him about this in writing, which is justified by Art. 382 of the Civil Code of the Russian Federation.

Typically, banks assign overdue loans at a price of one to ten percent of the debt amount, but, as a rule, wholesale debts cost that much; for a single percentage it can be higher. Particularly common are schemes for purchasing one’s own debts at a large discount after the bank’s license is revoked.